Understanding the Letter of Intent (LOI) in Real Estate Transactions

Introduction: The Role of an LOI in Real Estate

Navigating commercial real estate transactions can be a complex and multifaceted process. One document stands out for its ability to clarify intentions, streamline negotiations, and provide a roadmap for future agreements: the Letter of Intent (LOI) . Used widely by buyers, sellers, landlords, and tenants, the LOI is often the first formal step in a transaction, serving as a written summary of the major deal terms and setting expectations for both parties before a binding contract is drawn up [5] .

What is an LOI and Why Is It Important?

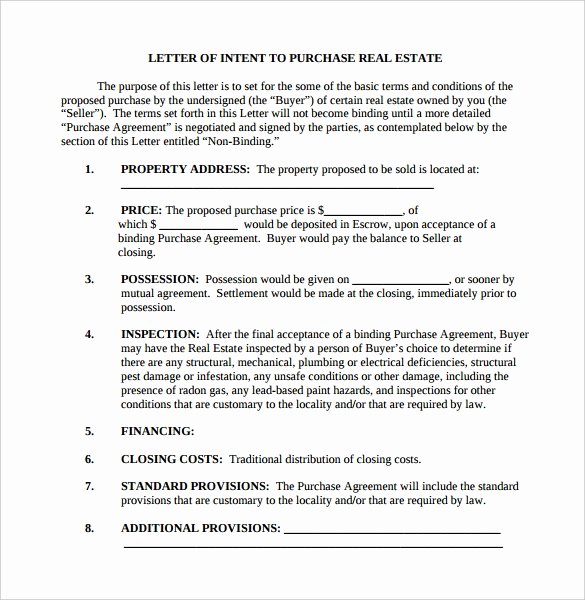

An LOI is a non-binding document that outlines the key terms of a potential real estate transaction, such as the purchase price, deposit amount, financing terms, due diligence requirements, and closing timeline [3] . Although it is generally not legally binding, parties may mutually agree that specific sections-such as confidentiality or exclusivity-are enforceable [1] . The importance of an LOI lies in its ability to:

- Document the foundational understandings between parties

- Minimize misunderstandings and wasted time

- Enable more efficient and focused negotiations

- Set expectations for the next steps in the transaction process

Key Elements Typically Included in an LOI

While every real estate deal is unique, most LOIs include the following elements:

Source: youtube.com

- Identification of the property : Clear description or address of the asset being sold or leased

- Purchase price or lease rate : Initial offer or range for the transaction

- Deposit amount : Proposed earnest money or security deposit

- Financing terms : Outline of the buyer’s financing structure or requirements

- Due diligence period : Timeline for inspections, appraisals, and review of property documents

- Closing date : Target date to finalize the transaction

- Contingencies : Conditions that must be met before closing, such as financing approval or environmental review

- Exclusivity and confidentiality : Provisions that may prevent parties from negotiating with others or sharing sensitive information

For commercial leases, the LOI may also address lease length, annual rent increases, tenant improvement allowances, free rent periods, and assignability [2] .

Step-by-Step Guidance: Drafting and Using an LOI

To effectively use an LOI in real estate, follow these steps:

- Research and Tour Properties : Before drafting an LOI, thoroughly research available properties and conduct site visits. This helps ensure your proposed terms are competitive and realistic [1] .

- Initiate Informal Discussions : Speak with owners, brokers, or landlords to understand their expectations and any unique aspects of the property or deal.

- Draft the LOI : Typically, the buyer’s or tenant’s broker prepares the LOI based on preliminary discussions. Use clear, concise language to outline all major deal points, referencing the elements listed above.

- Review and Negotiate : Share the LOI with the other party for review. Negotiate terms until both sides reach a mutual understanding.

- Sign the LOI : Although usually non-binding, signing the LOI demonstrates good faith and intent to proceed. Some markets require signatures from both parties before moving forward [2] .

- Move to Formal Agreement : After the LOI is signed, parties begin drafting a legally-binding purchase and sale agreement or lease contract.

If you are unsure how to draft an LOI, consider consulting a licensed real estate attorney or a commercial broker for guidance. Many local and state realtor associations offer sample LOI templates and legal resources.

Source: pinterest.com

Real-World Example: Commercial Property LOI

Suppose a buyer is interested in purchasing a multi-tenant office building. After touring the property and discussing basic terms with the seller’s broker, the buyer’s agent drafts an LOI that includes:

- Property address and description

- Offer price of $5 million

- Earnest deposit of $100,000

- 45-day due diligence period

- Contingency for financing approval

- Target closing date within 90 days

- Confidentiality provision

After mutual review and negotiation, both parties sign the LOI and proceed to draft a purchase and sale agreement, referencing the terms outlined in the LOI. This step helps prevent misunderstandings and ensures both sides are aligned before incurring significant legal and due diligence expenses [3] .

Potential Challenges and How to Address Them

While LOIs are valuable tools, certain challenges may arise:

- Binding vs. Non-Binding Terms : Parties should ensure the LOI clearly states which sections are binding and which are not. Legal review is recommended to avoid unintended obligations [2] .

- Ambiguous Language : Vague terms can lead to disputes. Detail all points with specificity.

- Changing Market Conditions : If market values shift before the final contract, parties may need to renegotiate terms. LOIs should include provisions for such scenarios.

- Counteroffers and Competition : Sellers and landlords often continue marketing properties after an LOI is signed. Buyers should clarify exclusivity terms if needed [2] .

To mitigate these challenges, use precise language, seek legal advice, and maintain open communication throughout the process.

Alternative Approaches and Best Practices

Some parties use term sheets instead of LOIs, which serve a similar function but may be less formal. In certain jurisdictions, parties may use a Memorandum of Understanding or Letter of Understanding [1] . Regardless of format, the goal is to clarify major deal points before committing to a binding agreement.

Best practices include:

- Consulting with qualified legal and real estate professionals

- Using sample templates from official realtor associations

- Reviewing recent market data to inform proposed terms

- Maintaining flexibility for changes during negotiation

How to Access LOI Services and Resources

To access LOI services and templates, consider the following steps:

- Contact your local or state realtor association for sample LOI documents and legal guidance.

- Consult a licensed real estate attorney for drafting assistance and legal review.

- Speak with commercial real estate brokers for market-specific advice and negotiation strategies.

- Use official platforms such as the National Association of Realtors or state real estate commissions for additional resources. Search for “commercial real estate LOI template” on their official websites.

- When purchasing or leasing property, request sample LOIs from your broker or agent as part of your due diligence process.

If you need further help, search for “real estate attorney” or “commercial real estate broker” using your preferred online directory or contact your local real estate board for recommendations.

Summary and Key Takeaways

The LOI is a foundational document in commercial real estate transactions, providing clarity, structure, and a basis for negotiation. While generally non-binding, it can include enforceable provisions if drafted accordingly. By thoroughly researching properties, consulting qualified professionals, and clearly outlining major terms, you can leverage the LOI to facilitate smooth and successful real estate deals.

References

- [1] Feldman Equities (2024). Why the LOI is One of the Most Important Documents in Commercial Real Estate.

- [2] CARR (2024). What Does Letter of Intent Mean?

- [3] Avenue Legal Group (2023). Letter of Intent in Real Estate Transactions.

- [4] Feldman Equities (2024). What is a Letter of Intent in Commercial Real Estate.

- [5] Sands Anderson (2025). What to Know About Letters of Intent in Real Estate and Business Deals.